Frictionless payments experiences powered by a modern, end-to-end payments technology platform.

Create seamless payment experiences with our powerful processing, proprietary gateway technology, and personalized support to help supercharge your growth from day one.

5AVERAGE RATING

GOOGLE REVIEWS

20+YEARS INDUSTRY EXPERIENCE

Headache-free merchant services that grow with you—and move you forward.

We understand that payment processing can be confusing, technical, and costly, and that you want a provider that has your best interests at heart.

Trusted across every industry, Fidelity offers a full suite of customizable payment solutions and one-on-one support to help you streamline your daily operations, fight fraud, lower costs and power your growth.

It's extremely rare these days to find an organization that truly understands client service. Thanks Josh and Team for putting us first and providing such a smooth seamless experience!

”

David J.

The future of integrated payments, today.

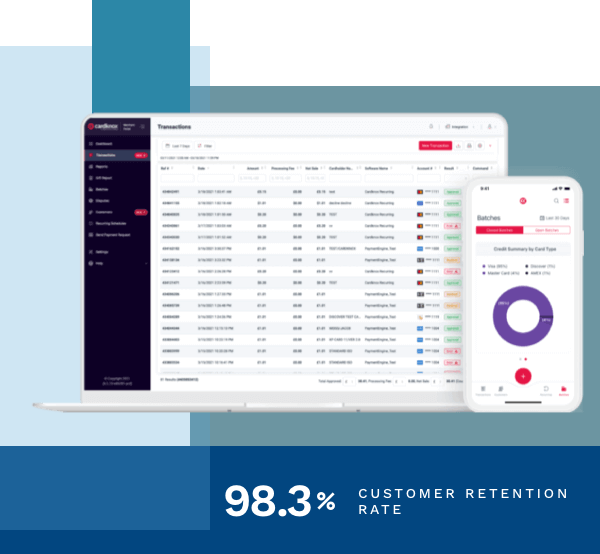

Cardknox is Fidelity’s end-to-end omnichannel technology platform and payment gateway.

Get ready for secure payments optimized for your industry.

Whether you accept payments in-person, online or via a mobile app, Cardknox provides you with one streamlined solution for the best in secure payments. Cardknox’s solution is designed with both customer and merchant in mind, and is the best solution for businesses and nonprofits alike. Enhance the customer experience, boost efficiency, and cut costs with a flexible and advanced secure payment solution.

Experience our powerful suite of omnichannel payment solutions.

Cardknox is the leading, developer-friendly payment gateway integration provider for in-store, online, or mobile transactions – hassle-free. No payment integration is too complex: Our solutions make even the most difficult integrations that much easier, so you can get exactly what you need in a lot less time.

Our team understands the complex and fast-changing world of payment services and puts that expertise to work every day to help your business thrive.

PERSONALIZED TECHNOLOGY SOLUTIONS

No one-size-fits-all solutions here. We give you the flexibility and control

to design your payment processing system around your business’s unique needs.

LOWEST RATES, NO HIDDEN FEES

Our unique IQM technology analyzes, monitors and optimizes every transaction to ensure you get the lowest possible rate, every single time.

24/7 HANDS-ON CUSTOMER SUPPORT

Questions? Our caring, knowledgeable, in-house experts will get you answers fast, so you can make the most informed decisions for your business.

Two Decades of Industry Know-How

Our team understands the complex and fast-changing world of payment services and puts that expertise to work every day to help your business thrive.

Personalized

Technology

solutions

No one-size-fits-all solutions here. We give you the flexibility and control to design your payment processing system around your business’s unique needs.

Lowest rates, no hidden fees

Our unique IQM technology analyzes, monitors and optimizes every transaction to ensure you get the lowest possible rate, every single time.

24/7 Hands-on Customer Support

Questions? Our caring, knowledgeable, in-house experts will get you answers fast, so you can make the most informed decisions for your business.

Industries We Serve

Health clubs Amusement parks & recreation center Cities & municipalities Zoos & wildlife Auto repair Grocery & supermarket Pharmacy Restaurant Car rental Apparel & fashion Jewelry Waste management And More…

Amazing experience! Michael guided me exactly to the services we needed, and got us fully up and running on schedule despite our very tight deadline. The pricing is super competitive, and the experience was a breeze.

I have spoken to one of your customer service representatives on several occasions, and she has been extremely helpful and professional. She is an asset to your company. I would highly recommend Fidelity in the future, due to my experience with your customer service team.

More Than I Could Ask For

As usual, your customer service team did more than I knew I could ask for--before I even asked.

More Than Satisfied

Every time we call your customer service department we are MORE than satisfied. As the customer service manager of our company, I would hire them on the spot.

Great service!

Knowledgeable, quick, responsible tech support. Highly recommend this company to anyone.

5-Star Recommendation

By FAR the best credit processor I've worked with (and I've worked with many).

Amazing Customer Service

Fidelity has an amazing customer service! It doesn’t matter how much business you do with them, they will always set you up as a priority customer.

Nothing short of amazing!

Fidelity Payment Services always answers my questions and are always willing to help. I highly recommend them for any of your processing needs.

Devotion and constant support

I am highly satisfied with Fidelity's services.Their staff is knowledgeable, professional and always available!

JOIN 25,000 BUSINESSES USING FIDELITY TO GET MORE DONE

Learn about industry trends, and get valuable business tips. Sign up to receive our emails!

By clicking 'Subscribe', you agree to our Privacy Policy.

Our website uses cookies to enhance website functionality and to provide you with the best possible website experience. To learn more about how we use cookies, please see our Privacy PolicyOkPrivacy policy

For Merchants

For Merchants For Developers

For Developers